Spotify

Welcome to the 175 subscribers who joined us in the last week. If you haven’t already, join 9,670 other business lovers and subscribe for free:

Today’s post is sponsored by Stratosphere.io. It’s a financial data platform that we use and it’s awesome for gathering and visualizing financial data for any company you’re researching.

Get started researching on the Stratosphere.io platform today, for free. And you can use the promo code: investingcity for 25% off your first year.

You know Spotify. It’s a music streaming business. But before getting into it, let’s jump in our time machine and understand the history of this industry.

HISTORY OF MUSIC

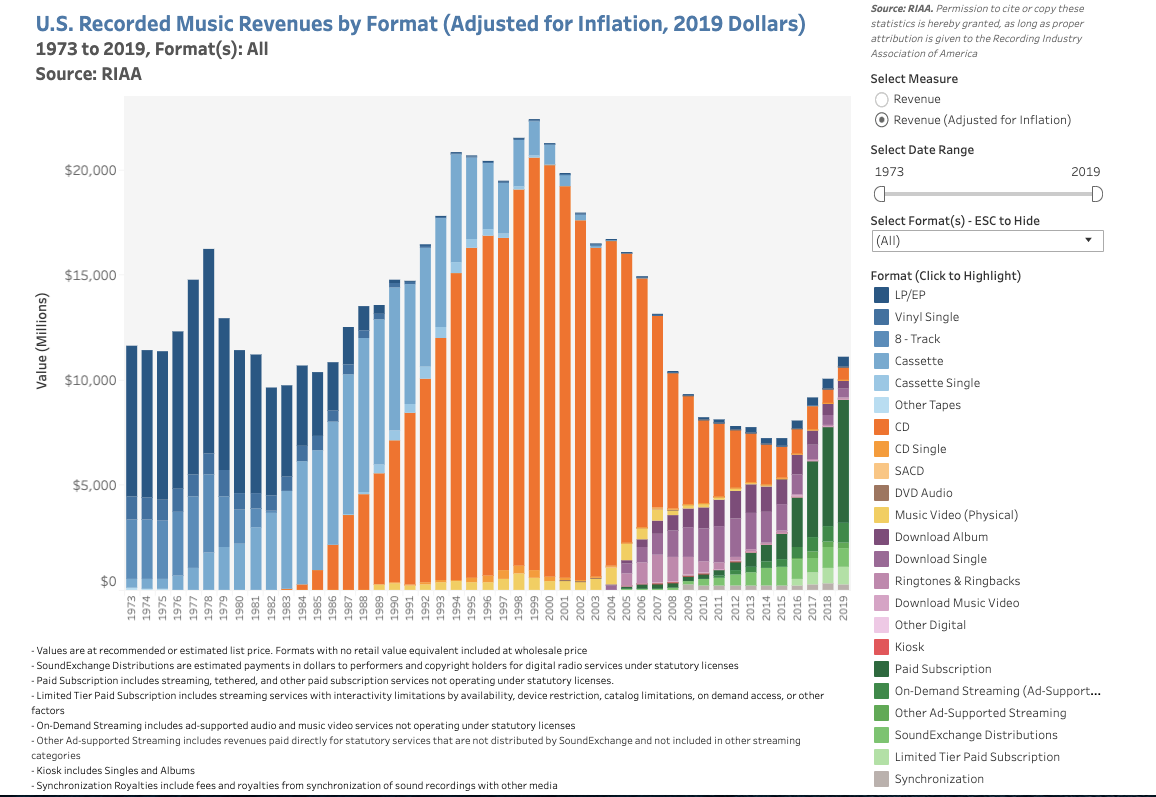

Prior to the invention of the phonograph (yes, we’re going ALLLLL the way back), the music industry consisted of sheets of paper. People would invite their friends over, and then the only way to listen to music was to literally play it, like on the piano. Then the phonograph and its associated technologies were created at the beginning of the 20th century. To be precise, the phonograph was invented by none other than Thomas Edison in 1877. Apparently it was his favorite invention (that’s really saying something considering his other inventions!).

Music could now be recorded. This created a whole new industry — the record industry. Scratch some music into vinyl and people were buying them like hotcakes (is that still a saying?). The first record label was Columbia Records which was actually borne out of the Columbia Phonograph Company. It had a local monopoly on selling Edison’s machines but this arrangement was later broken up. To sell more phonographs, Columbia contracted with a few opera singers to record some songs — voila, the first record label. After this, record labels had clout because distribution was so expensive. From recording the music, to creating the physical records, to getting them in record stores, to handling inventory and payments…you get the idea. Because of this, artists would typically only get 5-15%.

Then the medium changed. What was once vinyl, turned into cassette tapes, and then the almighty CD. By the 1980’s, there were six big record labels that survived each medium change — EMI, CBS, WEA, BMG, MCA, and PolyGram. These are the basis for today’s modern tri-opoly. Sony bought CBS in 1987 and later merged with BMG in 2004. In 1998, MCA and PolyGram merged to form what is now Universal Music Group (owned by French media conglomerate, Vivendi). And WEA stands for Warner-Elektra-Atlantic and is now Warner Music Group. Lastly, EMI was split between Sony and Universal some years later.

This consolidation and the fact that distribution was king led to the labels having a stronghold on the industry. Want to get on the radio? Need a label. Want to be on the Billboard 100? Label. Your songs used in commercials and movies? Label. You get the idea.

INTERNET WAVES

Enter the internet.

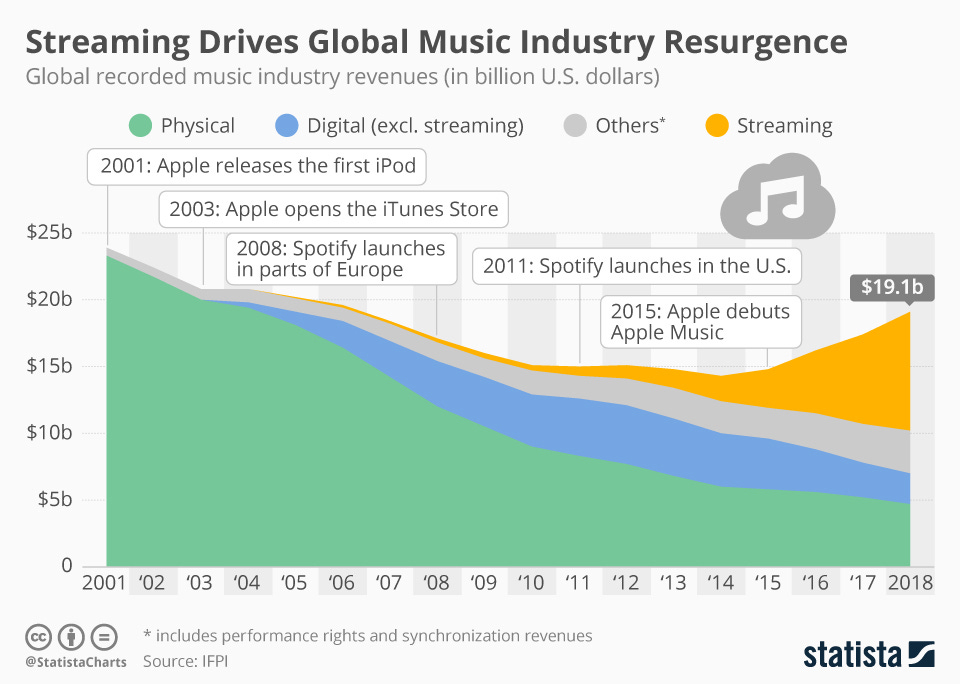

Napster is the poster-child for the demise of the music industry. From 1999 (when the company was founded) to 2014, US music industry revenues decreased collectively by more than 50%. It wasn’t until streaming really took off that the industry started growing again.

So where did all that money go?

Into the pockets of consumers actually. Gone were the days of buying an album for $30 when you could cherry-pick a song for 99 cents from iTunes.

And here’s where the story of Spotify picks up. In 2006, a 23-year Swede sold an ad-tech company, making him a millionaire. His name was Daniel Ek. Four years before this, Ek observed the downfall of Napster and knew that piracy would never be the answer. So after selling his company, he started Spotify in 2008. The timing turned out to be interesting. It was the midst of the financial crisis and the downward spiral of the music industry; perfect timing, right? Well, it actually worked to Ek’s advantage. Ek started the company in Sweden and started by approaching European labels, which didn’t have the same tri-opoly structure. These labels were dwindling and here was this start-up offering them cash for licensing deals. Even with the favorable set-up, it took Ek two years to sign deals with the European record labels. And not until July 2011 did Spotify officially launch in the US.

When Spotify came to the US, it already had over 1 million subscribers. Not a ton in the grand scheme of things, but enough to start doing some more licensing deals. Now, just 9 years later, the company has 286 million monthly active users. This has been the clear strategy — acquire users. With more and more users, the company has more negotiating leverage with the “Big Three.” Interestingly enough, Spotify now does more in revenue than Universal Music Group, which is the biggest of the record labels.

Out of the 489 million MAUs, 205 million are premium subscribers. However, premium subscriber revenue makes up 87% of sales. To be precise, the number of ad-supported MAUs is actually 163 million. The discrepancy is likely covered by the fact that around 7 million premium subs aren’t actually active on a monthly basis (130+163-7= 286). Spotify utilizes an ad-supported model as a customer acquisition tool. In fact, 60% of Spotify’s paying users first start out using the ad-supported freemium option.

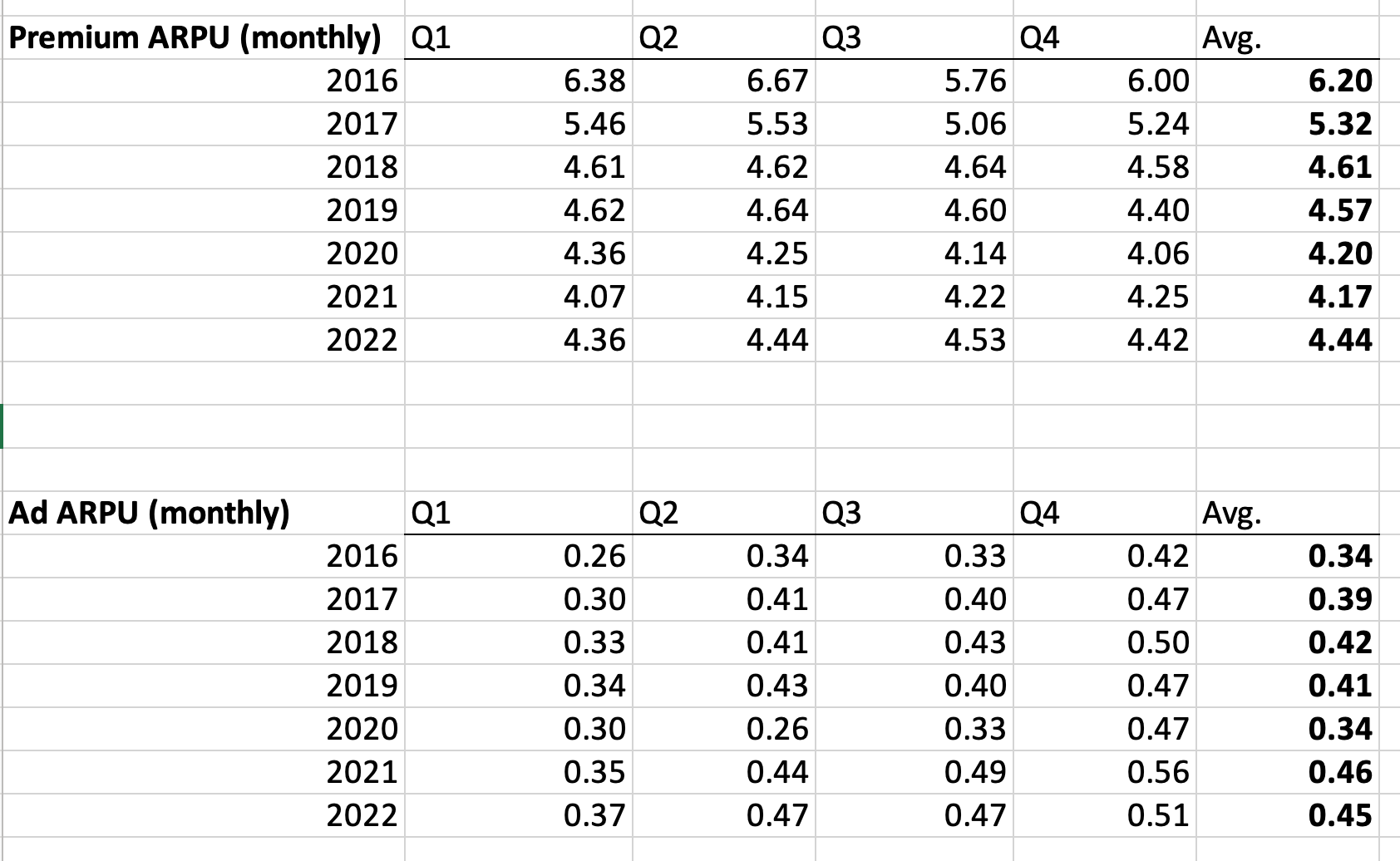

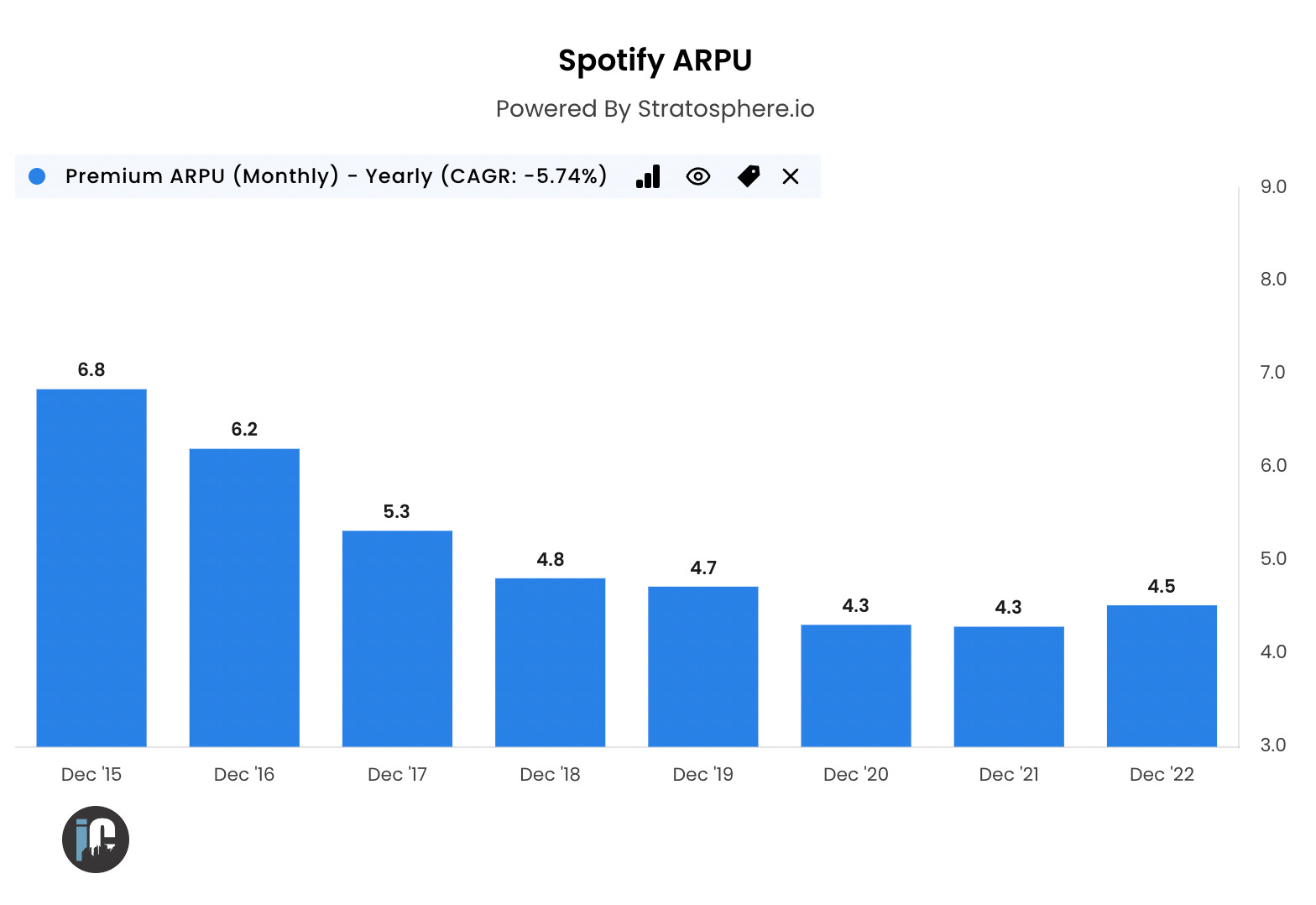

In US dollars, the company does around $11 billion in premium revenue and just under $1.6 billion in ad-supported revenue. If we divide those numbers by their respective user bases, we can get an average revenue per user within each segment. For the past 7 years, the ARPU numbers have been as follows:

And then if you blend those two, you get an overall ARPU number:

The first inclination is to think, “Wow, something is wrong, the company has no pricing power.” But again, the strategy has been to acquire subscribers. For instance, in 2019, the implied monthly cost is ~$5/month. But how can that be if Spotify costs $10/month? Well, there are a few reasons.

For one, that’s the price in the US. Much like Netflix, the company doesn’t charge the same in every country. Based on GDP/capita, this makes sense. Here’s a list of the latest prices by different markets:

Second, Spotify offers some different pricing options. It bundles Hulu + SHOWTIME for students at $5 month. Based on the revenue share agreements with those partners, it’s safe to say that Spotify hauls in a bit less than $5. But it’s a smart strategy. As soon as the student graduates, that’s a doubling in ARPU. And now s/he is hooked on Spotify. Third, another bundle is the family plan where it costs $15/month for up to 6 people. These three reasons are why the company’s premium ARPU numbers are so different from the US’s standard $10/month plan. In fact, it’s half of that.

MORE ON MUSIC

That’s the business model. But the reason for the big build-up and history lesson is to give insight into the margins. At 25% gross margins, most investors gawk. A tech company with 25% gross margins? What is this?

You remember the “Big Three” right? Universal, Sony and Warner. While the specifics of each contract are different, Spotify pays out about 70% of revenue for access to the labels’ backlogs (a backlog is all the songs/artists that the labels have copyright agreements with.) Spotify has gotten a lot of bad press in the past from artists complaining about how they don’t get paid enough on its platform. Reports suggest that artists get paid anywhere between $.006 and $.0084 for each stream. That means that an artist would receive $8,400 for every 1 million streams. At first glance, it seems like the artists have a point. But that ignores the very structure that underpins this whole thing — the labels. Spotify negotiates with the labels, not the individual artists. It's the labels that create the economics. And it’s not like Spotify is juicing them. A few years back Spotify had 15% gross margins for goodness sakes!

Compare this to the radio. Before getting into it, you need to understand that in songwriting, there are two copyrights: composition and sound recording. The former is the lyrics/melody and the latter is the actual audio. So if an artist hired a ghostwriter, the writer would have the composition rights and the artist would have the sound recording rights. In radio, only the composition rights are honored. But for some reason, in streaming services/internet music stations, both royalty streams must be paid out. It’s very bizarre. For some reason, because the music is being delivered by cable or via satellite, the sound recording has to be paid out as well. This sort of regulation basically screams that radio is dying.

In that light, it becomes clear that a lot of artists aren’t getting paid from radio royalties anyway. Even so, a radio play is much different than a Spotify stream. For one, 286 million people is quite the audience. In perspective, there are 1.4 billion cars in the world and a fraction of them are driving at the same time. All in all, Spotify compared to radio might actually be pretty fair. But that’s not what artists are comparing it to. They are comparing it to albums sold back in the good ole’ days. And people paying 99 cents for every song through iTunes. Of course, compared to that, Spotify is an unfair deal. But the distribution has changed forever. Streaming simply doesn’t cost NEARLY the amount that creating a physical record does. So why are artists REALLY upset? It doesn’t have anything to do with Spotify; it’s because they signed away a lot of their rights to the labels. I mean Sony’s music division has EBIT margins that are the same as Spotify’s gross margins. It’s clear that the labels have the best economics. But it’s a catch-22, because the labels do have a lot of marketing know-how and distribution muscle so it’s a default option for a lot of up-and-coming stars. Plus, it’s how the industry has always worked so I’m sure the successful artists just recommend that route to the newbies as it is the safest — e.g. would you rather have a little bit of a lot or a lot of nothing?

OTHER STREAMERS

Layer on top of this the music packages by Apple and Amazon. These are just more ways for the labels to monetize their backlogs. The more fragmentation in streaming, the better for labels. It means that one company doesn’t have leverage over them. But Spotify has emerged as a clear leader. For one, Apple Music reportedly has about half of the premium subscribers. And Amazon Prime has roughly 150 million total Prime members, which at 100% utilization is not much more than Spotify’s premium subs. Plus, music isn’t a big focus for these companies. Music is just another way to decrease churn.

One interesting example to look at is Pandora. It only has about 6 million premium subscribers (Spotify has 20x the subscriber base) and 65 million ad-supported ones. However, on that 65 million, it does more than $1 billion in advertising revenue, or 50% more than Spotify in that revenue segment. So that means that Pandora is monetizing its ads 50% more with less than half of the ad-supported users. Anyone who has used Pandora can attest to this.

FUTURE OF AUDIO

Ok, we’ve gone deep into music. But what will the future of Spotify look like?

It’s clear that music will be just one piece of Spotify’s game plan. The real vision is to be the global scale provider of audio consumption. Much like Netflix is that for video, Spotify wants to be that for audio. Here comes the important kicker — that means podcasts as well.

Over the past decade, podcast listenership has tripled. And Spotify has really been pursuing the opportunity. A couple years ago, the company spent about $400 million on three podcast-related acquisitions: Parcast, Gimlet and Anchor. The first two are media companies focused on creating high-quality podcasts and the third one is a platform that enables podcasters to create and host their own podcasts (it’s actually what we use for The Investing City Podcast). Spotify has mentioned that over 70% of its new podcasts came from Anchor or within its own ecosystem. Another development related to this is a change in the company’s accounting methods. Podcast production and related revenue will now be recognized under ad-supported. This is a hint of Spotify’s vision for podcasts. And, of course, Spotify locked down both Joe Rogan and Bill Simmons, and their incredibly famous podcasts, for well over $100 million. It’s clear that Spotify is serious about podcasting (I used the word 11 times in this paragraph alone!)

Importantly, advertising is fairly primitive in podcasting. A brand reaches out to a host and strikes up an agreement. Then the host reads off an ad in the beginning or the middle of a podcast. There’s limited geotargeting or personalization. It’s no wonder that the podcasting industry is much smaller than video, print or pretty much anything else. But, here’s my prediction — Spotify is putting itself in a position to be the Facebook of podcast advertising. It will be like the radio where the brand creates its own ad and then it’s played on the podcast. Except much more targeted than the radio since your phone has your exact location and preferences. There could be a self-service advertising platform on Spotify where brands choose demographics and criteria to maximize their ad dollars. And then ads would programmatically be slotted into podcasts. This would be a win-win for podcasters and brands as this arrangement would likely be revenue-maximizing for both parties.

This also solves a problem for Spotify. Under current agreements, labels get 70% of all streaming revenue. As Spotify grows bigger and has more leverage over the labels through original music and sheer number of users, it will likely be able to renegotiate some of these tough contracts. However, that’s not something to particularly rely on as an investment thesis. Plus, Spotify has made it clear that it is not trying to compete with labels (of course it has to say that, labels still have the power). But podcast advertising circumvents these agreements. It will create much more favorable economics and allow the company to even spend more for backlogs which will make the labels happy and further increase Spotify’s leadership.

LEVERAGE IS KING

At the risk of reducing Spotify into my limited framework, it’s quite an interesting exercise in gently using leverage over the years. This is Spotify’s competitive advantage.

Step 1: Use the crisis in music as leverage to get licensing deals with fragmented European labels

Step 2: Use those licensing deals to expand internationally

Step 3: Play nice with the labels and give them good deals to increase premium subscriber base

Step 4: Leverage the subscriber base to get slightly better deals with labels and expand into podcasts

Step 5 (has not yet occurred): Leverage podcast revenue to further extend audio leadership and renegotiate with labels

TAKING THE OTHER SIDE

One thing to point out is that music and video are different. People replay their favorite songs much more than they watch their favorite movies. 4 minutes is just very different than 90 minutes of commitment. Therefore the backlogs are more important in music. If Step 6 of the exercise in leverage is to copy Netflix’s strategy of originals, it likely won’t have the same effect. That would be clear warfare on the labels which would then play hardball by upping revenue shares or collaborating to create their own service. Right now, the labels are happy because Spotify is growing ~ 20% and that is essentially accruing to them with generous cash advances. But to create real leverage Spotify could start signing on tons of new artists, bypassing the need for a label. Because once again, the distribution has changed. The labels are not nearly as important as they once were. But to Spotify they still are. Those backlogs are very sought-after because people like listening to their favorite songs.

[And here is a conspiracy theory but Spotify’s suggested songs could be a way to introduce subscribers to songs that they would like but are not under strict label agreements.]

CONCLUSION

Spotify is an interesting business to study because the bear cases are so often thrown around. Too many competitors, no differentiation, labels have too much power. While there are certainly grains of truth in them, the future of the company is exciting. Spotify has changed how music is distributed and while the economics are still representative of the old days, the future will likely be different based on Spotify’s amazing use of gentle leverage.

What Else We Offer

For self-directed investors: Dynasty Membership

Long-biased fund: Infuse Partners (intro call)

More content (The Investing City Podcast, online course, and blog)

Good and very structured write-up, covering the most important points. Thank you very much.

This is your best one yet. well done.